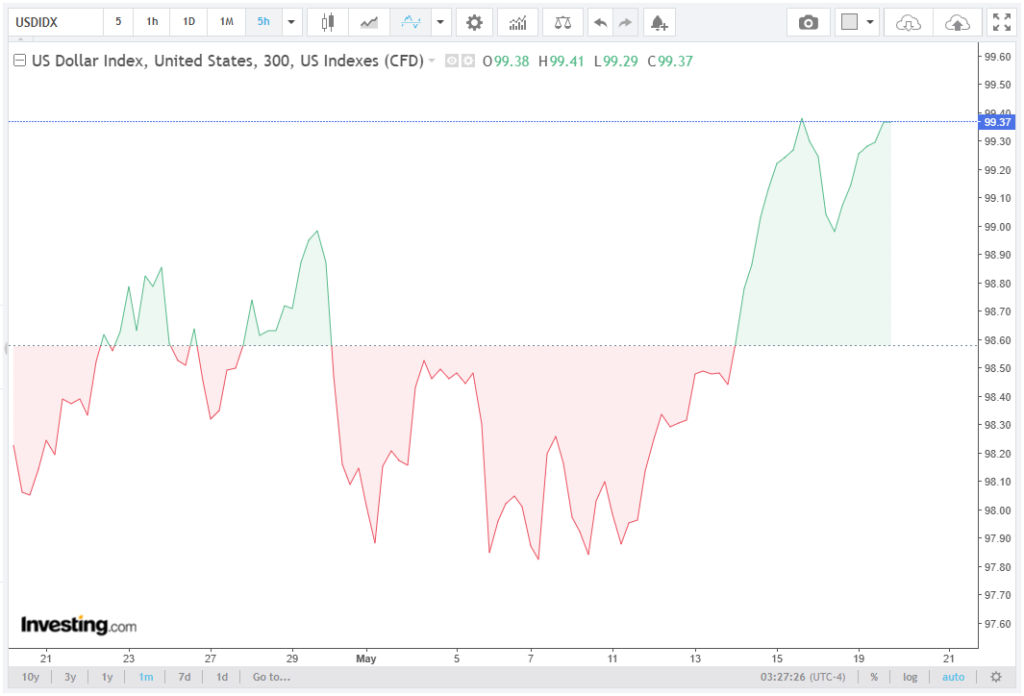

The US Dollar Index (DXY), which measures the strength of the USD against key global counterparts, rose for a second consecutive day, approaching a six-week high of 99.43, first seen during Asian trading on Tuesday. Analysts point to the continued upward momentum as a sign of investor confidence in the USD amid ongoing global economic developments.

The Greenback’s recent strength is underpinned by heightened risk aversion, inflation concerns, and volatility in the US Treasury market. Murrius Group brokers provide valuable perspectives and detailed commentary on this subject in their latest article.

Geopolitical Tensions and Market Risk Sentiment

Renewed threats of military action in the Middle East have intensified demand for safe-haven assets. Market participants priced in the potential for escalated conflict, which has reinforced the USD’s role as a defensive currency.

The geopolitical environment has also contributed to elevated volatility in oil futures, with Brent crude trading above $87 per barrel, up nearly 4% over the past week. The sustained upward pressure in energy prices feeds into expectations of persistent inflation, which in turn supports interest rate-sensitive assets such as the USD.

Risk aversion in global markets has resulted in cross-asset repricing, where equities have experienced mild declines while government bond yields and the DXY have advanced. Investors are increasingly factoring in the potential duration and severity of conflict, which could influence supply chains, commodity prices, and inflation dynamics in the medium term.

Treasury Yields and USD Dynamics

The US 30-Year Treasury Yield retreated slightly to 5.189% following a near 19-year peak of 5.200%, indicating a minor pullback in response to short-term risk-off positioning. The 10-Year Treasury Yield remained elevated at 4.687%, close to a 16-month high, while the 2-Year yield held near 4.139%, reflecting persistent pricing of tight monetary policy.

The movements in long-dated yields suggest that markets are assessing inflation persistence, economic growth expectations, and geopolitical risk premiums. The spread between the 2-Year and 10-Year yields remains inverted relative to historical averages, signaling continued market caution regarding future economic growth and potential monetary policy adjustments.

The combination of high yields and elevated risk aversion has directly supported the DXY. Historically, the index tends to appreciate when Treasury yields rise in tandem with global uncertainty, as investors seek the relative safety and return offered by USD-denominated assets.

Inflation and Monetary Policy Outlook

Recent energy price spikes have amplified expectations that the Federal Reserve may maintain a restrictive stance for longer than previously anticipated. With core inflation hovering near 3.9% year-on-year and headline inflation supported by energy and food prices, the Fed’s target range of 2% remains a distant reference point, reinforcing market expectations of prolonged high policy rates.

Monetary policy is currently considered mildly restrictive, exerting downward pressure on inflation while maintaining a stable labor market. The federal funds rate is positioned to apply moderate restraint, with room for further adjustments if economic growth exceeds potential or if inflationary pressures intensify. This stance has contributed to strong USD performance relative to currencies from regions with lower interest rate expectations.

USD Index Technical Drivers

The DXY’s recent surge has been driven by a combination of Treasury yield differentials, risk-off flows, and safe-haven demand. On a technical basis, the index is approaching resistance at 99.50, a level not seen in six weeks, with support observed near 98.80. Volatility in the DXY has increased, with the 14-day Average True Range (ATR) rising to 0.42, reflecting market sensitivity to both geopolitical and macroeconomic data releases.

FX market participants are particularly focused on the correlation between USD strength and Treasury yields, as widening yield differentials reinforce the carry advantage of USD assets. The interplay between geopolitical risk premiums and interest rate expectations has created an environment in which the USD retains structural support, despite periods of short-term retracement.

Implications for Global Markets

The combination of geopolitical escalation, elevated energy prices, and persistent Treasury yields is exerting upward pressure on the USD. This dynamic has implications for emerging market currencies, which have experienced increased depreciation pressures, as well as for commodity-linked currencies, which are sensitive to energy price shocks.

For the fixed-income market, the near-term decline in the 30-Year yield following its multi-year high may provide temporary relief for duration-sensitive portfolios, but the overall yield structure remains elevated. The inverted yield curve continues to signal potential growth moderation, reinforcing the USD’s safe-haven appeal.

Overall, the DXY’s position near six-week highs reflects the interplay of elevated geopolitical risk, persistent inflation expectations, and restrictive monetary policy, providing both a technical and fundamental basis for continued USD resilience. Market participants should monitor Treasury yields, energy prices, and FX volatility as key indicators for potential further upside in the index.