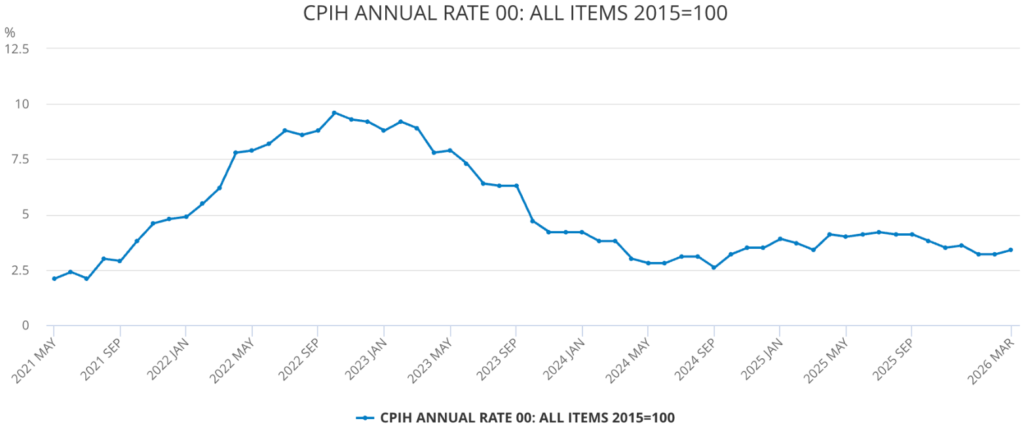

The United Kingdom (UK) Consumer Price Index (CPI) for April showed a moderate easing in inflationary pressures, with headline CPI rising 2.8% year-over-year (YoY), down from 3.3% in March. Market expectations had anticipated a 3.0% YoY increase, indicating that inflation is slightly softer than projected.

Despite this moderation, the headline rate remains above the Bank of England’s (BoE) 2% target, reinforcing the central bank’s continued focus on price stability. Murrius Group brokers share expert insights and detailed analysis in their latest publication.

Monthly CPI growth remained at 0.7% in April, matching March’s monthly pace but below the market consensus of 0.9%, suggesting that short-term inflation momentum has slowed.

The core CPI, which excludes volatile food and energy prices, increased 2.5% YoY, down from 3.1% in March, and slightly below the 2.6% forecast, reflecting a softening in underlying inflation across goods and services.

April CPI: Dissecting the Numbers

The headline CPI decline of 0.5 percentage points compared to March represents the largest monthly YoY deceleration since mid-2021. The core CPI moderation from 3.1% to 2.5% YoY is the slowest pace for underlying inflation since July 2021, indicating that price pressures outside of food and energy are gradually easing.

Energy prices contributed significantly to the deceleration. Following a reduction in the Ofgem energy price cap, domestic electricity and gas prices increased at a slower rate than in previous months, limiting the impact of global energy cost shocks on consumers.

Seasonal factors also played a role, with the Easter period price distortions observed in March unwinding in April, contributing to a 0.2 percentage point drag on monthly CPI growth.

The food component of CPI, while still elevated at 4.2% YoY, showed signs of moderation from March’s 4.5%, reflecting a combination of stabilizing commodity prices and lower transportation costs. Housing costs, including rental and mortgage components, continued to exert upward pressure, with imputed rents rising 3.0% YoY, slightly below the March figure of 3.1%.

Producer Price Trends

The Producer Price Index (PPI), released alongside CPI, provides insight into upstream inflationary pressures. April’s PPI Input is forecast to slow sharply to 1.0% YoY, down from 4.4% in March, reflecting reduced costs of raw materials, metals, and intermediate goods.

PPI Output is expected to tick up modestly to 1.0% YoY, compared with 0.9% in March, suggesting that finished goods pricing is stabilizing, with firms absorbing a portion of cost pressures rather than passing them entirely to consumers.

The moderation in both input and output PPI aligns with the softening CPI trajectory, signaling that inflation pressures may be contained in the near term. However, the upcoming July revision of the Ofgem energy price cap is projected to increase domestic energy bills by approximately 15-20%, likely driving headline CPI back toward 4% by late 2026.

GBP/USD Market Response

The GBP reacted modestly to the CPI release, with the GBP/USD pair down 0.10%, trading at 1.3381. Technical indicators show the Pound is under pressure after a recent sell-off, despite a minor short-term bounce.

Resistance levels are observed at 1.3450, with mid-May highs around 1.3530-1.3540 representing potential upside if broader sentiment improves. On the downside, immediate support is at 1.3305, with a break below that level exposing late March and early April highs near 1.3175.

The CPI moderation may temporarily alleviate market expectations for aggressive BoE action, providing a slight bullish bias for the Pound. However, the combination of domestic political uncertainty, future energy price shocks, and structural GBP weakness will likely maintain near-term volatility.

Outlook for Upcoming CPI Reports

Looking ahead, the May CPI is expected to reflect a continuation of the current trend, with headline inflation projected at 3.0% YoY and monthly growth potentially rising slightly to 0.9%. Core CPI is expected to remain around 2.6% YoY, indicating subdued price growth outside energy and food categories.

Analysts will closely monitor the impact of the July energy price cap and services sector inflation, as these components are expected to drive future CPI dynamics.

Conclusion

The UK’s headline CPI of 2.8% YoY in April, alongside core inflation at 2.5%, signals a temporary easing of inflation pressures while remaining above the BoE target. The monthly CPI of 0.7% suggests short-term moderation, but upcoming energy price adjustments and supply-side pressures are likely to reassert upward pressure later in 2026.

For the GBP/USD, this translates into short-term volatility, with potential support from softer inflation tempered by structural weaknesses and geopolitical risks. The BoE is likely to maintain a cautious policy stance, using the easing in headline and core CPI as a window to assess the broader economic environment before taking further action.