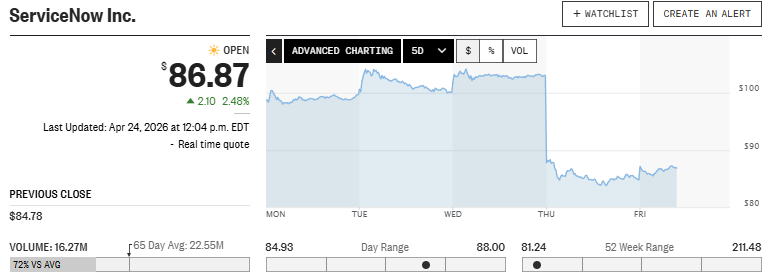

The enterprise software sector experienced a significant tremor on Thursday as ServiceNow shares collapsed by approximately 18% following the release of its first-quarter earnings report. This sharp retracement was triggered by a combination of downward price target revisions and investor anxiety regarding near-term margin pressure.

Despite the headline-grabbing drop, the underlying conflict remains between institutional bulls who view the sell-off as a rare entry point into a durable compounder and skeptics who are increasingly wary of the organization’s current acquisition-heavy strategy.

According to an investment analyst at Kixy, while the financial results were technically robust in several categories, the market reacted punitively to a 75 basis point drag on subscription revenue caused by the slippage of large on-premise deals in the Middle East.

This geopolitical timing issue, coupled with the capital intensity of the $7.75 billion Armis acquisition, has led to a flurry of revised outlooks from major investment banks.

Generative AI Traction And The Now Assist Pivot

The central pillar of the bull case remains the company’s rapid monetization of generative AI tools. Management recently elevated its target for “Now Assist” annual contract value (ACV) to $1.5 billion, signaling that the organization is successfully converting AI interest into realized revenue.

This “system of action” approach allows enterprises to automate complex workflows directly through the platform, positioning the firm as a primary beneficiary of corporate AI budgets throughout 2026.

Subscription revenue for the most recent period grew by 21% year-over-year to reach $3.466 billion, while current remaining performance obligations (cRPO) climbed 25% to $12.85 billion.

These metrics indicate that the core demand for the platform remains healthy, despite the geopolitical friction created by specific deal delays. However, observers point to the fact that cRPO upside was narrower than in previous quarters, suggesting that the explosive growth seen in early 2025 may be normalizing.

Acquisition Strategy And Margin Compression

The aggressive expansion into security and data governance has required significant capital outlays. In addition to the Armis deal, the company is moving forward with the integration of Moveworks and a pending acquisition of Veza.

These moves are designed to build a comprehensive “end-to-end” AI workflow platform, yet they have simultaneously induced margin compression that the market found difficult to ignore. Operating guidance was subsequently lowered to account for these integration costs, providing a primary catalyst for the share price decline.

Maintaining institutional-grade productivity amid such a rapid expansion is a complex task. To offset some of this volatility, the board authorized an additional $5 billion in share repurchases in January, reflecting a belief that the equity is undervalued relative to its long-term potential.

With free cash flow reaching $2 billion, the firm has the liquidity to support its dual strategy of aggressive M&A and shareholder returns, even if the near-term share price remains under pressure.

Valuation Debate And Upcoming Catalysts

Even after the 18% plunge, ServiceNow trades at a price-to-earnings ratio of approximately 60x, keeping the valuation debate alive. Some analysts argue that at 5x estimated 2027 revenue, the stock is historically cheap for its growth profile, while others caution that the software sector as a whole is undergoing a fundamental re-rating.

Morningstar has maintained its fair value estimate at $165.52, suggesting that the current market price near $85 represents a substantial disconnect from the underlying asset value. All eyes are now focused on the May 4 analyst day.

This event is widely expected to serve as the next major catalyst where leadership can address concerns regarding AI monetization, the post-acquisition roadmap, and the timeline for closing the stalled Middle Eastern contracts. A successful presentation could provide the “floor” the stock needs to begin its recovery process.

The Future of Enterprise Software: Outlook & Insights

The current volatility in ServiceNow’s stock highlights the high expectations placed on AI leaders in the current economic cycle. As the focus shifts from theoretical potential to tangible quarterly margins, operators must demonstrate an ability to scale through acquisitions without diluting core profitability.

We are entering a phase where institutional-grade productivity will be measured by the seamless integration of disparate data security tools into a unified AI workflow engine. Success for the remainder of 2026 will be determined by the organization’s ability to stabilize its margin trajectory following the heavy spending of the first quarter.

While the future expectations for the platform remain ambitious, the longer-term positioning of the organization as an AI “system of action” provides a more compelling growth narrative than most legacy software peers.

Ultimately, the financial trajectory of the enterprise market suggests that the current correction may be a necessary recalibration of growth expectations rather than a fundamental impairment of the business model.