Oracle just posted the kind of earnings report that forces analysts to revise their models upward. The enterprise technology giant beat expectations across the board for its third quarter, with revenue and earnings per share both growing over 20% year over year.

Finance expert at BUCKSA explores what these numbers actually mean for Oracle’s competitive position in AI cloud infrastructure and why one specific data point buried in the report may be more important than the headline results.

The Headline Numbers

Oracle’s third quarter delivered a clear beat on every major metric Wall Street was tracking. Total revenue came in at $17.19 billion, a 22% increase year over year and above the analyst consensus estimate of $16.89 billion. Adjusted earnings per share were $1.79, beating the expected $1.70. The company described the quarter as exceptional in its own reporting language, which for a company as measured in its communications as Oracle, carries genuine weight.

Cloud revenue was the standout, growing 44% year over year to $8.9 billion. That kind of growth rate in a segment generating nearly $9 billion per quarter is genuinely notable. It reflects strong demand from enterprises moving workloads to the cloud and, increasingly, from AI-related infrastructure projects requiring large-scale compute capacity.

The RPO Number Is the Real Story

The figure that deserves the most attention is not in the income statement at all. Oracle’s remaining performance obligations, which represent contracted future revenue not yet recognized, rose 325% year over year to $553 billion. That jump is staggering and represents a massive pipeline of committed business sitting ahead of the company.

Remaining performance obligations are one of the best forward-looking indicators of a software and cloud company’s revenue trajectory. When that number grows by 325%, it tells investors that Oracle is not just executing well today. It is locking in business at a pace that will sustain strong growth for years ahead, providing revenue visibility that most companies in any sector would envy.

AI Infrastructure Is Driving Demand

Oracle has made a deliberate strategic bet on becoming the third major cloud provider, with a specific emphasis on AI training infrastructure. Its Oracle Cloud Infrastructure platform has attracted enterprise clients and large AI companies looking for competitively priced cloud compute capacity.

The 44% cloud growth rate puts Oracle’s cloud business growing faster than both AWS and Microsoft Azure on a year-over-year basis. In a market where AI spending is projected to reach $520 billion in hyperscaler capex in 2026, even a growing share of that spend represents enormous revenue potential for a company positioned the way Oracle currently is.

What the Market Reaction Tells Us

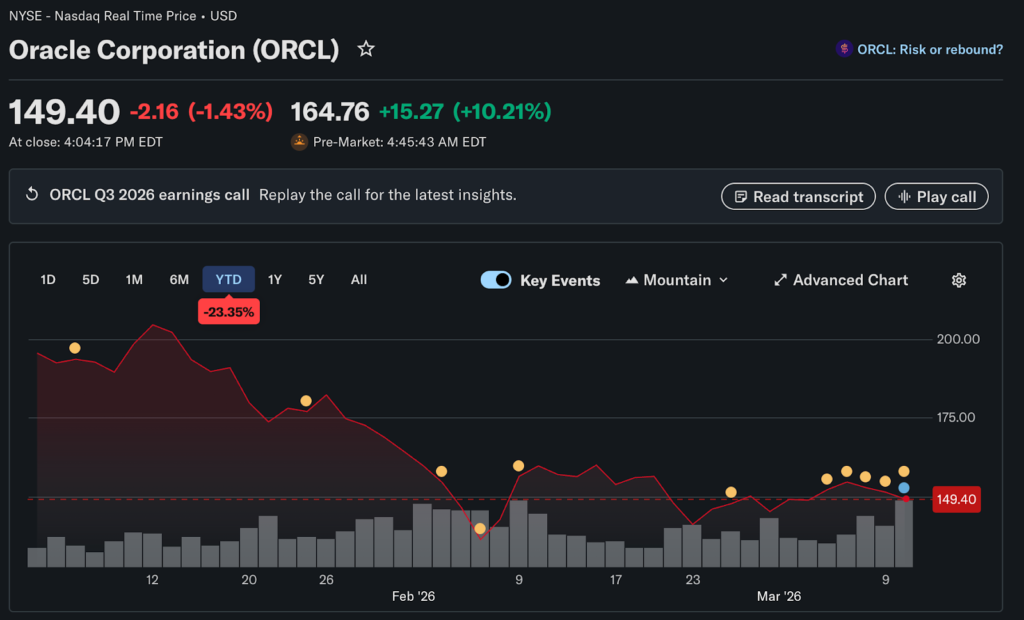

Despite the strong results, Oracle’s stock faced some selling pressure in the aftermath. The stock was down 1.43% on Tuesday according to market data, reflecting the broader market’s cautious tone rather than any specific concern about Oracle’s business fundamentals.

Investors focused on the RPO growth of 325% and the 44% cloud revenue expansion likely viewed any pullback as an opportunity. Short-term reactions in a volatile environment driven by oil price swings often say more about macro sentiment than about the company at the center of the trade.

The Software Upgrade Tailwind

The timing of Oracle’s results coincided with Deutsche Bank Research upgrading software stocks to overweight on Tuesday. The firm cited evidence that concerns about AI disruption to software businesses may have peaked, and that software stocks outperformed last week even amid broader market turmoil.

That sector-level tailwind adds context to how Oracle’s results may be received by institutional investors in the coming days. When a sector gets upgraded at the same time a major company in that sector posts strong numbers, the combination tends to attract meaningful buying interest from portfolio managers looking to reposition.

Oracle’s Strategic Position in 2026

Oracle’s ability to post these numbers during a period of significant macro uncertainty demonstrates the strength of its multi-year cloud transition. The company has spent over a decade migrating its historically on-premise enterprise software business toward cloud delivery, and the results show that transition is accelerating rather than plateauing as some analysts feared.

The $553 billion RPO figure is the clearest signal available that Oracle’s growth story is not a one-quarter phenomenon. It reflects a structural shift in enterprise spending toward cloud and AI infrastructure that is still in its relatively early stages.

What Comes Next

Oracle also raised its total revenue guidance for fiscal year 2027 to $90 billion, reflecting management confidence in the visibility provided by that RPO backlog. The combination of strong current results and a sharply upward-revised forward outlook positions Oracle as one of the more compelling earnings stories in enterprise technology for the remainder of 2026.

Investors watching AI infrastructure plays through the lens of software rather than hardware would be well served to track how Oracle’s cloud bookings continue to develop over the coming quarters.