The US Consumer Price Index (CPI) for February is anticipated to show a continued stabilization in inflation, signaling minimal surprises for markets closely monitoring the Federal Reserve’s (Fed) policy trajectory. This article contains a full breakdown of the topic prepared by the team at BlitzPine Group.

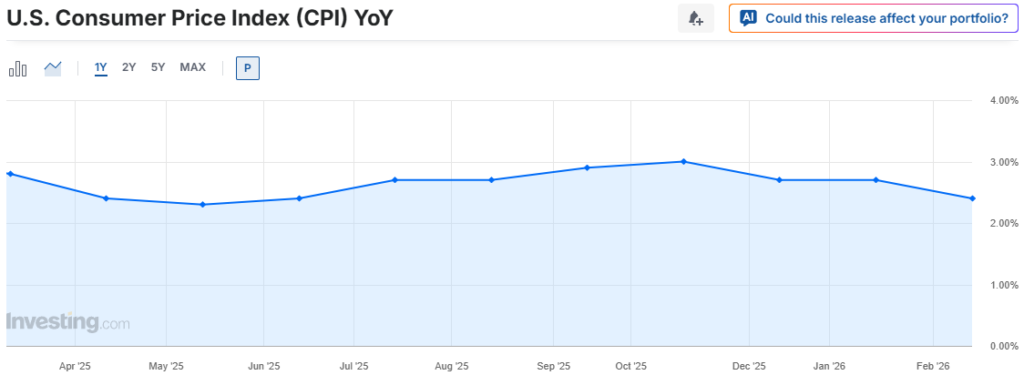

According to projections, the headline CPI is expected to rise 2.4% year-on-year (YoY), while the annual core CPI, which excludes volatile food and energy prices, is forecast to hold steady at 2.5% YoY. Investors and analysts are particularly focused on these readings as they provide critical insight into the Fed’s potential interest rate decisions in the coming months.

February CPI Preview: Stabilization Amid Energy Volatility

The US Bureau of Labor Statistics (BLS) is scheduled to release the February CPI data on Wednesday. Market expectations indicate a stabilization of inflation just above the Fed’s 2% target. While headline CPI may slightly accelerate to 0.25% month-on-month (m/m) due to a rebound in energy prices, the core CPI is expected to moderate to 0.23% m/m, reflecting a slower rise in services inflation and a more subdued tariff pass-through.

Despite recent geopolitical tensions, notably the US-Israel military operation against Iran, which caused West Texas Intermediate (WTI) crude oil prices to spike from $67 to over $110 per barrel before correcting, February CPI figures are unlikely to fully capture this energy shock. Consequently, market reactions may remain muted, as the inflation data does not yet incorporate the full effects of these developments.

Recent Inflation Trends and Input Price Pressures

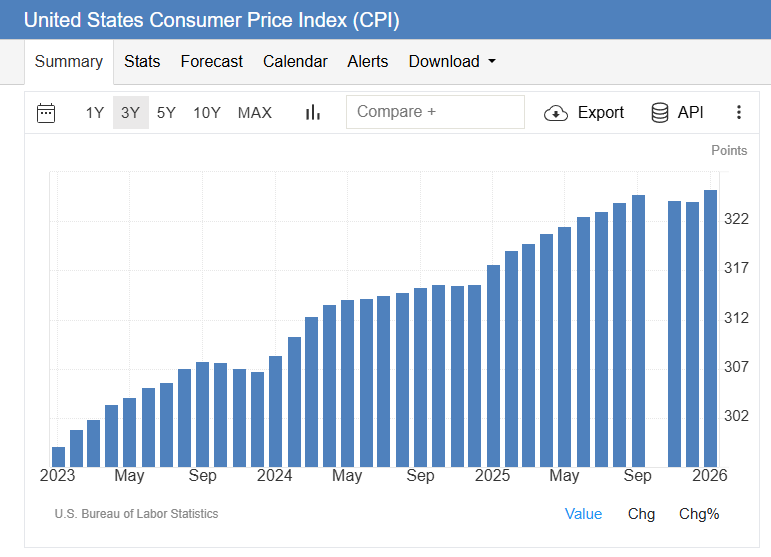

An examination of prior CPI releases shows a relatively consistent monthly pattern, with core CPI readings fluctuating between 0.2% and 0.3% m/m over the past six months, except for a 0.4% increase in August 2025. Headline CPI similarly remained in the 0.2-0.3% m/m range during this period.

Additional insight comes from the Institute for Supply Management (ISM) surveys. The Prices Paid Index in the Manufacturing PMI jumped to 70.5 in February from 59 in January, suggesting rising input cost pressures in the private sector. Conversely, the Services PMI Prices Paid Index fell to 63 from 66.6, indicating a softening in service-related inflation. Analysts at TD Securities note that these trends could point to moderation in services inflation, potentially boosting confidence in the FOMC’s cautious approach.

Market Implications and Fed Rate Expectations

Markets currently discount almost no chance of a Fed interest rate cut in March, with only a 12% probability of a 25 basis points (bps) reduction in April, according to the CME FedWatch Tool. Following the Fed’s decision to maintain rates in January, the likelihood of a fourth consecutive policy hold in June briefly rose to 70% after geopolitical concerns in the Middle East, but has since declined below 60% due to soft labor market data and easing crude prices.

A significant deviation in the core CPI reading, particularly a 0% m/m or lower print, could prompt markets to reassess June rate cut probabilities, placing downward pressure on the US Dollar (USD). Conversely, a stronger-than-expected 0.3% m/m core CPI could reinforce the case for continued policy restraint, providing support to the USD.

EUR/USD Technical Outlook Amid CPI Anticipation

FX markets are closely watching EUR/USD, which shows signs of a bearish bias despite a recent rebound. According to Eren Sengezer, FXStreet European Session Lead Analyst, the Relative Strength Index (RSI) on the daily chart has rebounded from near-30 but remains below 50, suggesting that a bullish reversal has not yet materialized.

EUR/USD remains capped beneath the 1.1675–1.1700 resistance band, an area strengthened by several technical indicators, including the 200-day Simple Moving Average (SMA), the 61.8% Fibonacci retracement of the November–January rally, and the 100-day SMA. If buyers are unable to push the pair back above this region, the next downside levels to monitor appear around 1.1600–1.1590, which aligns with the 78.6% Fibonacci retracement, followed by a deeper support zone near 1.1500–1.1470, close to where the broader uptrend originally began.

The CPI data release is unlikely to trigger a dramatic EUR/USD movement unless there is a substantial surprise, given current market pricing for Fed policy actions.

Conclusion

The February US CPI report is expected to confirm a steady inflation environment, providing the Fed with evidence of stabilization. While headline and core CPI are projected to remain within expectations, ongoing energy price volatility and geopolitical uncertainty are likely to influence market sentiment and FX movements in the coming months. Investors should focus on core trends in services inflation and monitor any unexpected deviations that could alter the Fed’s policy outlook and the US Dollar’s performance.