The closure of the Strait of Hormuz is now in its third week as of March 16, 2026. The conversation in financial markets has moved beyond the initial price shock and into territory that most oil-price analyses do not typically address. Finance experts atNoxi Rise have been examining the second and third-order consequences of the disruption, and those consequences extend considerably further than crude benchmarks suggest.

Roughly 20% of global petroleum consumption was used to transit the Strait before the conflict. The US military struck Kharg Island, Iran’s primary oil export hub, over the weekend. Further strikes on energy infrastructure have been threatened. Commercial traffic through the waterway has been substantially interrupted.

The Price Story in Context

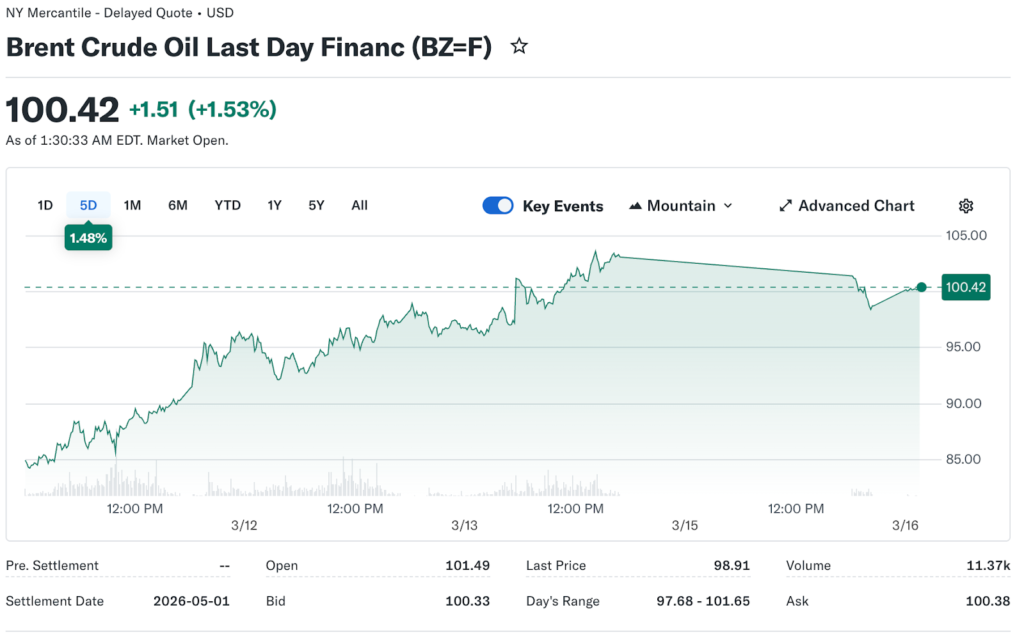

Brent crude posted week-to-date gains exceeding 11% through March 14. WTI briefly spiked to $119 per barrel before retreating below $100. Those headline numbers have dominated financial coverage, but the spot price trajectory only tells part of the story.

Long-dated oil futures have begun pricing in disruption through Q3 2026. That is the more significant market signal. When futures markets three to six months out start embedding supply disruption, corporate hedgers respond by locking in current rates. That hedging activity itself maintains price pressure even during periods when spot prices temporarily pull back. The forward curve has become a self-reinforcing mechanism.

What Shipping Insurance Is Revealing

Marine insurance premiums for vessels attempting or even approaching the region have surged significantly. Underwriters at Lloyd’s and competing syndicates have added substantial war risk premiums to coverage for Middle Eastern routes. Some carriers have suspended regional operations outright. Others are rerouting around the Cape of Good Hope, adding weeks to delivery times and dramatically increasing operational costs.

Those rerouting costs do not appear in oil price charts. They appear in shipping earnings reports, freight indices, and eventually in the cost of imported goods across Europe and Asia. Retailers, manufacturers, and distributors that rely on the timely delivery of components or finished goods are already modifying procurement strategies.

The Refinery Margin Problem Nobody Is Talking About

European and Asian refineries that have historically processed Iranian and Gulf crude blends are now sourcing alternative feedstocks at premium prices. Those refineries are built and calibrated for specific crude grades. Switching feedstock is possible but creates processing inefficiencies that reduce throughput and increase per-barrel costs.

That margin compression at the refinery level gets passed downstream. Fuel prices at the pump reflect crude costs, but they also reflect refinery margins. The refinery squeeze in the current environment means that consumer fuel prices could remain elevated even if crude prices pull back meaningfully from recent highs.

The Coalition Plan and What It Would and Would Not Fix

The US has signaled plans to announce a multi-national coalition to escort vessels through the Strait of Hormuz. If implemented effectively, that plan could restore commercial shipping confidence and trigger a $20 to $30 correction from recent crude price highs.

But Noxi Rise finance experts caution that a coalition announcement would not immediately resolve the economic damage already in motion. Inflation expectations are already embedded in pricing models across industries. Supply chains have begun adjusting to alternative routes. Companies that locked in higher energy and shipping costs during the spike will not unwind those contracts overnight. The downstream cost effects persist well beyond the moment when the headline threat is removed.

The Goldman Sachs Warning That Should Be Getting More Attention

Goldman Sachs has warned that rising energy costs tied to the conflict could reduce global GDP by 0.3% and increase headline inflation by up to 0.6% if conditions persist. Those numbers might appear modest in isolation, but they land in an economy where growth was already softening, and inflation was already proving sticky.

A 0.3% GDP reduction in a low-growth environment is the difference between expansion and contraction in several major economies. A 0.6% increase in headline inflation is enough to push central banks back toward caution at exactly the moment they were preparing to ease. The interaction between those two effects is what makes the current energy shock particularly difficult for policymakers to manage.

Three Metrics for Monitoring the Situation

The finance experts at Noxi Rise are tracking three specific data points to gauge how the disruption evolves. First, Strait of Hormuz transit volume, tracked in real time via shipping analytics providers. Any increase in commercial traffic would signal improving conditions ahead of official announcements. Second, US crude inventory builds, which indicate whether alternative supply is arriving fast enough to offset lost flows. Third, refinery utilization rates in Europe and Asia, which reveal whether the feedstock switching costs are being managed or expanding.

The oil story is not finished. The market is still finding its pricing level for a world where one of its most critical shipping routes remains contested.