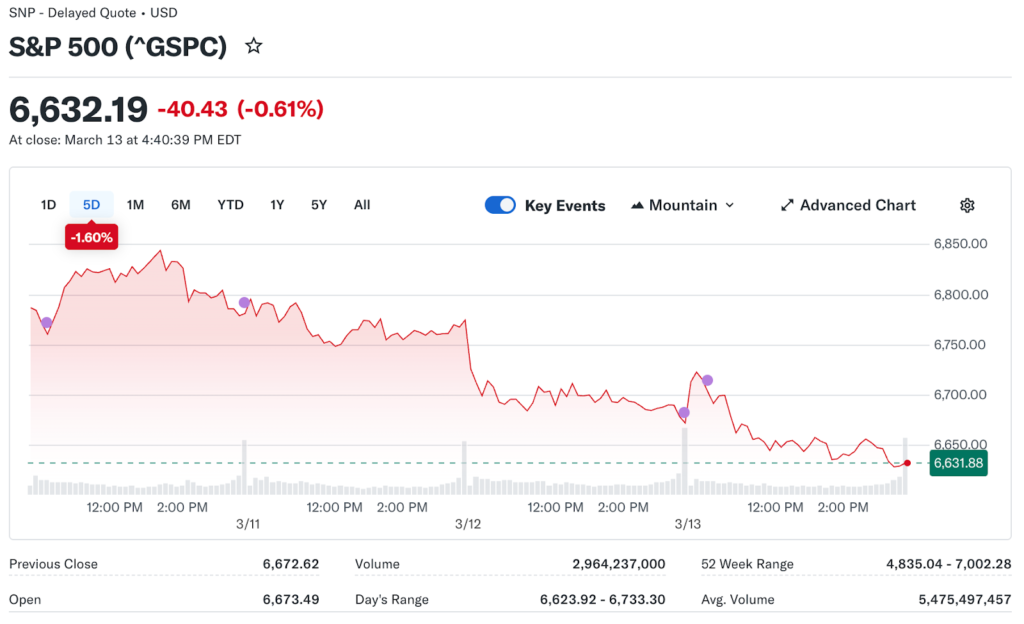

The S&P 500 opened March 16, 2026, hovering near 6,656 points, recovering slightly from the fresh 2026 low set just days before. Three consecutive weeks of losses have reset the mood across institutional trading desks. The S&P 500 lead financial expert atNoxi Rise says the streak is more than a statistical footnote: it reflects a genuine repricing of the macro environment that investors had been slow to absorb.

Last week, the Dow fell 1.99%, the S&P 500 dropped 1.6%, and the Nasdaq Composite shed 1.26%. It was the first three-week losing streak in approximately a year for all three major benchmarks simultaneously.

The Week That Put the Streak in Motion

The numbers from March 13’s session are worth reviewing in detail. Salesforce fell 3.25%. Apple lost 2.15%. Microsoft dropped 1.57%. Those are not small-cap names experiencing sector-specific pressure. They are the core holdings of passive index funds and institutional equity portfolios globally.

On the winning side, Boeing gained 2.56%, UnitedHealth rose 1.79%, and Verizon added 1.42%. The distinction between winners and losers is not random. Defense, healthcare, and telecom holding up while software and consumer technology fall is the signature pattern of a risk-off rotation into defensive positioning.

What a Three-Week Streak Signals to Institutional Traders

Most market participants treat a single bad week as noise. Two weeks get flagged. Three weeks trigger a strategy review at the most serious institutional desks. The pattern that emerges from three straight weeks of losses often determines whether firms reduce equity exposure in their model portfolios for the quarter ahead.

Fund managers who entered 2026 positioned for continued growth and a rate cut cycle are now sitting with positions that no longer match the macro environment they were sized for. The adjustment process typically takes weeks, not days. That means continued selling pressure from rebalancing is likely even if the headline news flow stabilizes.

The Adobe Situation Deserves More Attention

Adobe’s 7.6% drop following its earnings report has been treated primarily as a company-specific story. It deserves a broader reading. Adobe beat earnings forecasts. The stock still fell sharply. The reason was the abrupt departure of a chief executive with an 18-year tenure, arriving at a time when the company’s AI competitive strategy is under active pressure from newer entrants.

The market’s reaction illustrates a pattern specific to this environment. In a risk-off period, investors penalize uncertainty more heavily than they reward outperformance. A company can deliver strong numbers and still lose market cap if investors cannot confidently model the strategic path forward. That dynamic is particularly acute for software companies, where competitive moats depend heavily on product vision and leadership continuity.

How the Energy Sector Is Leading for the Wrong Reasons

The energy sector’s year-to-date outperformance is worth interpreting carefully. It is leading the S&P 500 not because the economy is growing and industrial demand is rising, but because oil supply has been disrupted by the Strait of Hormuz closure. Those are fundamentally different drivers.

Energy leading from supply disruption typically does not signal broad economic health. It reflects a wealth transfer from energy consumers to energy producers within an otherwise weakening growth environment. Portfolio managers who see energy’s outperformance and interpret it as a bullish macro signal are reading it incorrectly.

WTI briefly hit $119 per barrel before pulling back below $100. That spike, even if temporary, raises operating costs for airlines, shippers, manufacturers, and retailers simultaneously. The downstream impact on corporate earnings will not show up until the first-quarter results begin reporting in April. By then, the damage will already be done.

Consumer Behavior Is Already Shifting

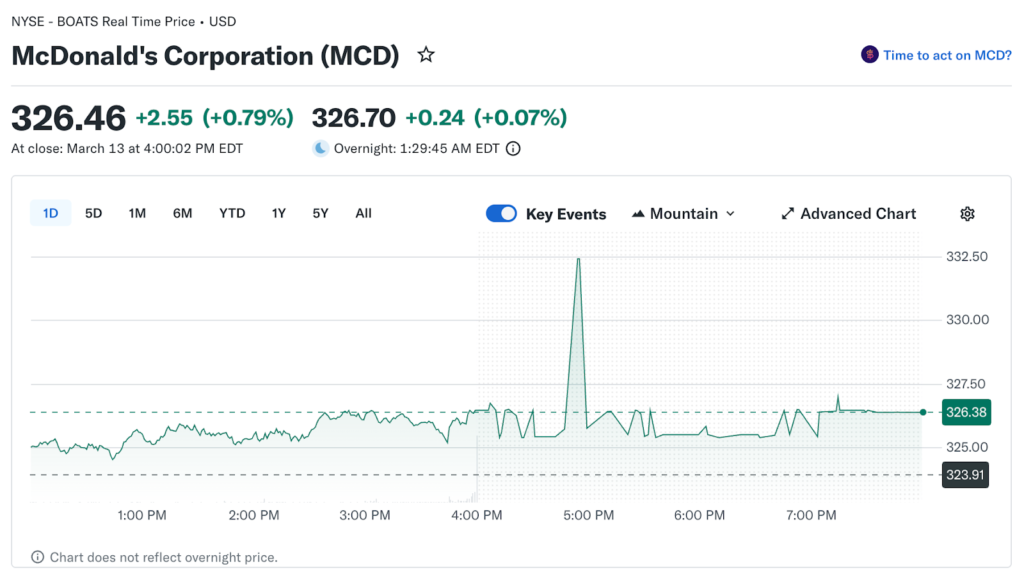

McDonald’s shares are down more than 4% month to date, even as management prepares to refresh its value menu with a $4 breakfast bundle launching in April. Starbucks, by contrast, is up 18% year to date and gained 1.8% in March, suggesting that while budget-conscious spending is under pressure, premium daily habits are proving more durable.

That divergence reflects a familiar split in consumer behavior during uncertain periods. Spending that feels like a treat or a ritual holds up longer than spending that feels like a routine cost. The data point is small but consistent with broader consumer sentiment research showing that households protect discretionary rituals even when they cut back on discretionary spending overall.

Three Things That Would Change the Trend

Noxi Rise’s lead financial expert identifies three developments that would alter the current market trajectory. A credible resolution plan for the Strait of Hormuz that restores shipping confidence. A Federal Reserve dot plot on Wednesday that preserves at least one rate cut signal for 2026. And a stabilization in oil prices below $90 per barrel on a sustained basis.

Until those three conditions arrive, the path of least resistance remains lower. Investors chasing a bottom here are likely early. The market tends to stop falling when bad news stops surprising people, and the bad news has not stopped yet.