Japanese equities surged to historic highs at the start of the week, with investors reacting positively to a decisive national election outcome that reinforced expectations for policy continuity and fiscal expansion.

The rally pushed benchmark indices into uncharted territory, underscoring renewed confidence in Japan’s medium- to long-term growth outlook. Market analysts at Rovex Markets note that the scale of the move reflects both political clarity and sustained momentum in domestic equities.

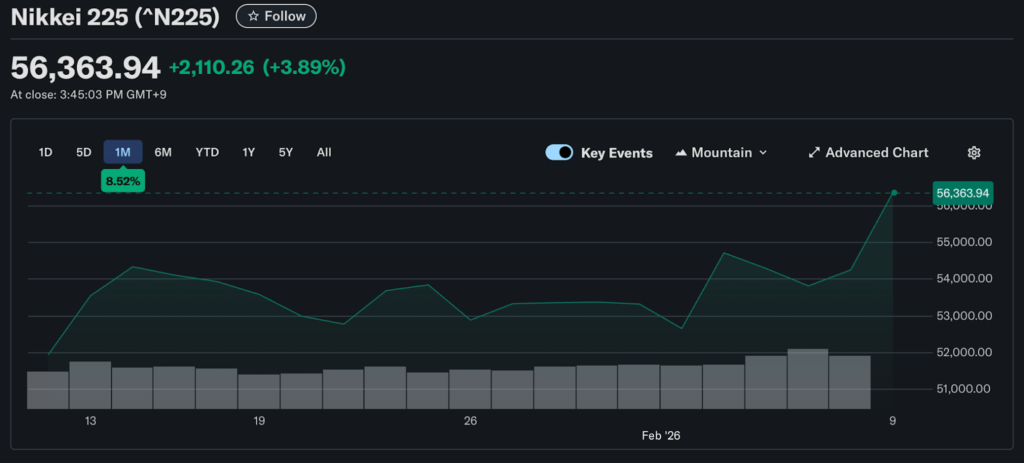

The Nikkei 225 index briefly crossed the 57,000 level for the first time on record, before trimming gains to close 3.9% higher at 56,363.94. The broader Topix index also reached an all-time high, finishing the session up 2.3% at 3,783.94. The synchronized advance highlighted broad-based participation across sectors, rather than a rally concentrated in a narrow group of stocks.

Election Outcome Strengthens Market Confidence

The market reaction followed confirmation that the ruling party secured a two-thirds supermajority in the 465-seat lower house, delivering a clear and stable governing mandate. Investors interpreted the result as a material reduction in political uncertainty, while strengthening the administration’s ability to advance fiscal initiatives, tax reform, and long-term investment programs.

Such clarity is particularly significant in Japan’s political landscape, where coalition dynamics and legislative gridlock have historically constrained policy execution. With a strengthened mandate, expectations have grown that structural reforms and public spending plans can proceed with fewer obstacles and delays.

Policy Expectations Drive the Momentum Trade

Japanese stocks have posted multiple record highs in recent months, driven by expectations that current leadership will pursue proactive fiscal policy, encourage corporate investment, and maintain accommodative monetary conditions. These expectations have supported risk appetite, particularly among domestic investors, who have steadily increased equity exposure.

The policy outlook is widely seen as supportive of corporate earnings growth, while also exerting downward pressure on the yen, a combination that historically benefits export-oriented companies. Although currency moves were more measured in the latest session, the broader policy narrative continues to favor equities over defensive assets.

Bond Yields and Currency Signals

Following the equity rally, movements in other asset classes reflected recalibrated expectations rather than risk aversion. The Japanese yen strengthened modestly to around 156.88 against the U.S. dollar, signaling ongoing sensitivity to capital flows and interest rate differentials.

Meanwhile, government bond yields edged higher. The 10-year Japanese government bond yield rose nearly 4 basis points to 2.274%, while 20-year yields climbed approximately 3 basis points to 3.158%. The increase in yields indicates that markets are beginning to price in a more assertive fiscal stance, with higher issuance and stronger growth expectations influencing long-term rates.

Despite the rise, yields remain low by historical standards, preserving supportive financial conditions for equities.

Regional Markets Follow Japan Higher

The rally in Tokyo spilled over into other Asian markets, reinforcing the perception that Japan’s political clarity has broader regional implications. South Korea’s main index surged more than 4%, reflecting strong gains in technology and industrial stocks. Smaller-cap shares also advanced sharply, signaling improving regional risk sentiment.

In Australia, the benchmark index closed 1.85% higher, supported by strength in financials and resource stocks. Hong Kong’s main index gained more than 1.7%, while mainland Chinese equities also moved higher, with key benchmarks posting gains above 1.4%.

Global Context Adds to Momentum

The upbeat tone in Asia followed a strong end to the previous week in U.S. markets, where major indices staged a rebound after a period of volatility. The Dow Jones Industrial Average closed above 50,000 for the first time, while the S&P 500 and Nasdaq Composite posted gains of nearly 2% and above 2%, respectively.

Although weekly performance in the U.S. remained mixed, the rebound helped stabilize global risk sentiment. Investors appeared more willing to re-engage with equities, particularly in markets offering policy visibility and valuation support.

Implications for Japanese Equities

The break above 57,000 on the Nikkei represents more than a symbolic milestone. It reflects a reassessment of Japan’s long-term growth potential at a time when other major markets face slowing momentum and tighter financial conditions.

Corporate governance reforms, shareholder-friendly policies, and rising domestic participation have all contributed to the rally. The election result adds another layer of confidence by reducing policy uncertainty and improving execution credibility.

Outlook for Markets

Looking ahead, Japanese equities appear well supported by a combination of political stability, policy continuity, and favorable financial conditions. While near-term volatility cannot be ruled out, the broader trend remains constructive as long as growth-oriented policies remain intact.

For global investors, Japan’s performance underscores the importance of political clarity in shaping market outcomes. In an environment where uncertainty dominates many regions, decisive mandates and predictable policy frameworks continue to attract capital and support equity valuations.