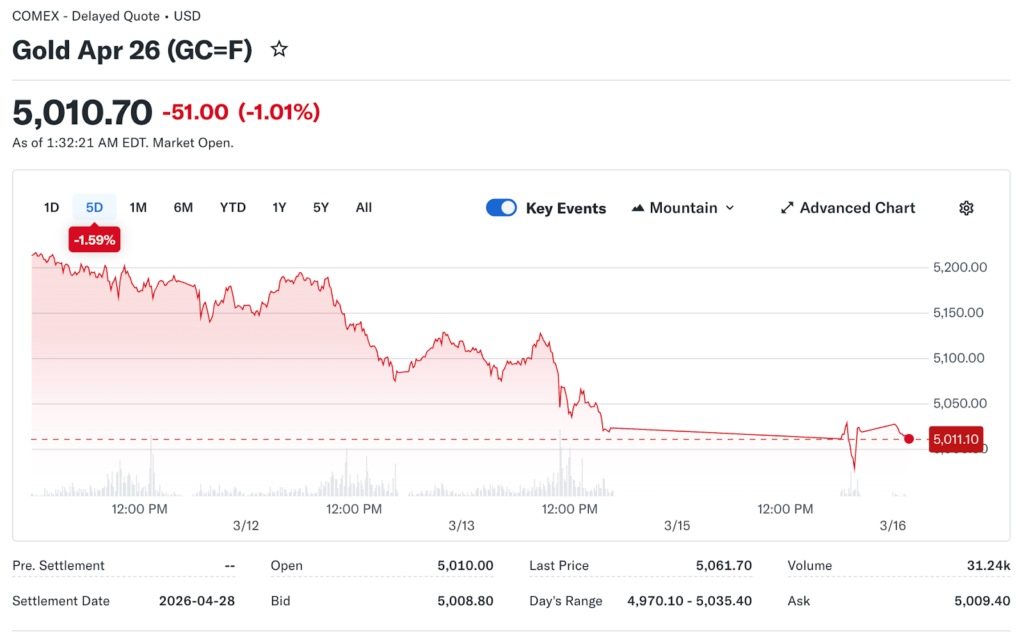

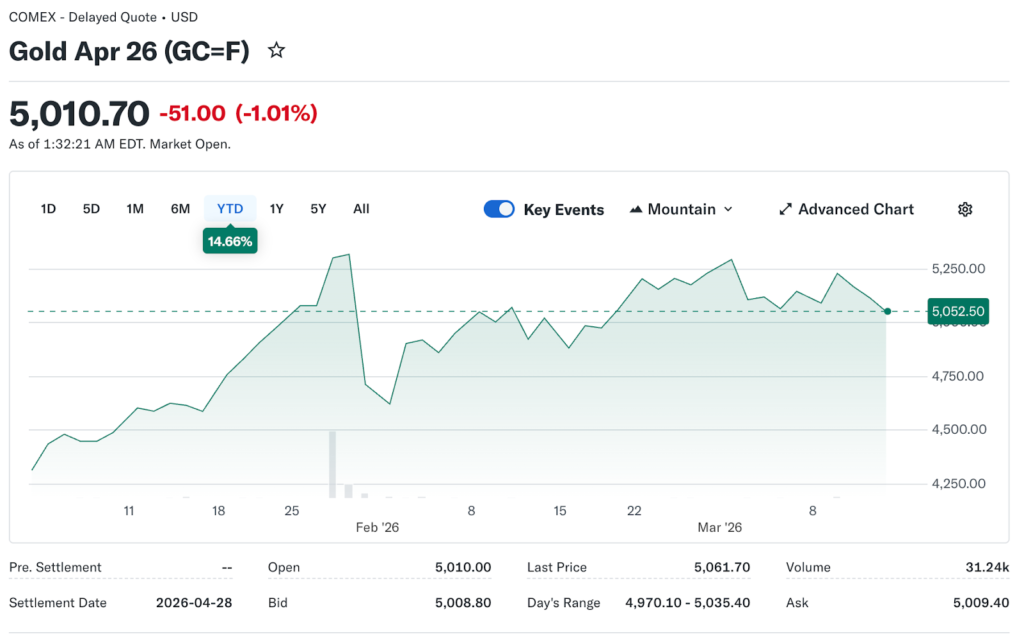

Gold is holding above $5,000 per ounce as markets open on March 16, 2026, and the more telling detail is not the price itself but where support is building. Senior brokers atNoxi Rise have been watching the metal’s floor level rise consistently over the past six weeks, and they say that pattern tells a different story than a standard safe-haven spike driven by a single event.

Most geopolitical price spikes in gold reverse within weeks once the acute fear subsides. This one is being reinforced by multiple independent drivers. That distinction changes how investors should be thinking about position sizing and time horizon.

The Numbers on the Ground

Gold is consolidating between $5,052 and $5,208 as of this week’s early sessions, according to technical forecast models. Key support sits at $4,996 on the downside, while resistance is clustered around $5,266. Analysts with more aggressive outlooks are citing potential targets of $5,426 if the current structure holds and geopolitical conditions do not ease rapidly.

The downside scenario for a reversal places the first meaningful floor near $4,821. Notably, the floor level itself has been rising. Four weeks ago, the equivalent floor estimate was several hundred dollars lower. An upward-drifting support level is the clearest sign of a genuine structural repricing rather than a temporary sentiment move.

Why Standard Rate Logic Is Not Working Here

Under normal conditions, gold weakens when interest rate cut expectations fade. The Federal Reserve has pushed the first expected cut out to December 2026, down from earlier forecasts of multiple cuts earlier in the year. By conventional logic, that rate timeline should be weighing on gold. It is not.

Core producer prices rose 0.8% in January, the strongest monthly gain since mid-2025. That reading strengthened the dollar and pushed rate cut expectations back further. Gold barely blinked. When an asset fails to respond to a catalyst that should push it lower, it tells experienced traders that something structural is holding the bid.

That structural bid comes from a convergence of forces. Rising energy-driven inflation. Universal 10% tariffs imposed through Section 122, with the potential to rise to 15% following a new Supreme Court ruling. Persistent geopolitical uncertainty with no clear resolution timeline. Each of those drivers has its own momentum independent of Federal Reserve policy.

Central Banks and the Institutional Demand Story

Retail investors buying gold out of fear get most of the media coverage. The institutional and sovereign demand side is considerably more relevant to price sustainability.

Central banks globally have been accumulating gold reserves at rates not seen in decades. Sovereign wealth funds, particularly across Asia and the Gulf region, are holding and in many cases expanding positions. This demand is not reactive to current events. It reflects a multi-year strategic recalibration of reserve asset allocation away from excessive dollar concentration.

That diversification trend was already in motion before the Iran conflict began. The conflict has accelerated it, but did not create it. Even if the Strait of Hormuz situation resolves in the coming weeks, central bank demand does not reverse on that timeline. It is a structural bid that will persist regardless of near-term geopolitical outcomes.

The Capital Rotation Confirming the Gold Move

A large-scale rotation out of equities and into long-term US Treasuries has been visible in the data over recent weeks. That move pushed 10-year bond yields to a four-month low. When both bonds and gold rise simultaneously during an equity selloff, the message is clear: capital is seeking preservation over return.

That dynamic is different from a typical risk-off trade where investors move to cash or short-term bills. Moving into long-duration bonds alongside gold signals a willingness to accept low but certain returns while avoiding exposure to equity volatility and inflation-sensitive corporate earnings. It is the portfolio positioning pattern of genuine uncertainty rather than tactical caution.

The Tariff Variable That Is Still Being Underpriced

Most gold analysis is currently focused on energy prices and the conflict. The tariff story deserves more weight. Universal 10% tariffs on imports raise consumer prices independently of oil. They affect manufacturing costs, retail goods, and supply chain margins. Combined with energy inflation, the two mechanisms create an inflationary environment that is broader and stickier than either would produce alone.

If tariffs rise to 15% as signaled, the inflation outlook becomes materially worse. Gold historically benefits when inflation is perceived as structural rather than transitory. The tariff escalation makes the structural case considerably stronger.

What Happens Next

Senior Noxi Rise brokers note that four drivers are simultaneously sustaining gold’s move: the Iran conflict, tariff-driven inflation, fading rate cut expectations, and institutional reserve diversification. Each has a different resolution timeline. The conflict could end in weeks. Tariff policy moves on a legal calendar. Central bank strategies unfold over years.

Until at least two of those four factors shift meaningfully, gold’s structural support is intact. The $5,000 level is no longer a ceiling being tested. It has become a reference point that the market is building above.